The invention of several new technologies and the transformation into digitalisation have dynamically changed the process of many sectors and now the Insurance sector is next in the row. The Insurance Regulatory and Development Authority of India (IRDAI) advocated adopting "Telematics for Motor Insurance" in a new proposal a few months ago, so soon our driving habits will have an impact on the cost of our auto insurance.

Fleet Companies spend a lot of money on insurance, so telematics insurance is becoming a means of reducing costs. Smaller fleets typically pay Rs. 80,000 annually for each vehicle, but big truck fleets may spend Rs. 1,20,000 or more. On average according to data, telematics insurance may reduce those expenses by 10% to 15%.

You may be wondering what Telematics Insurance is and how does it work?

Insurance based on data obtained from a vehicle is known as telematics insurance. Data from a vehicle's mileage, frequent destinations, and harsh driving behaviors including hard breaks, acceleration, airbag deployment etc. can all be included. Insurance companies use the data from the vehicle to calculate the offers and discounts they may give a business. Fleets that travel shorter distances, for instance, could be offered a better bargain than those that travel farther. Fleets with safety equipment may be eligible for greater savings than fleets without such features.

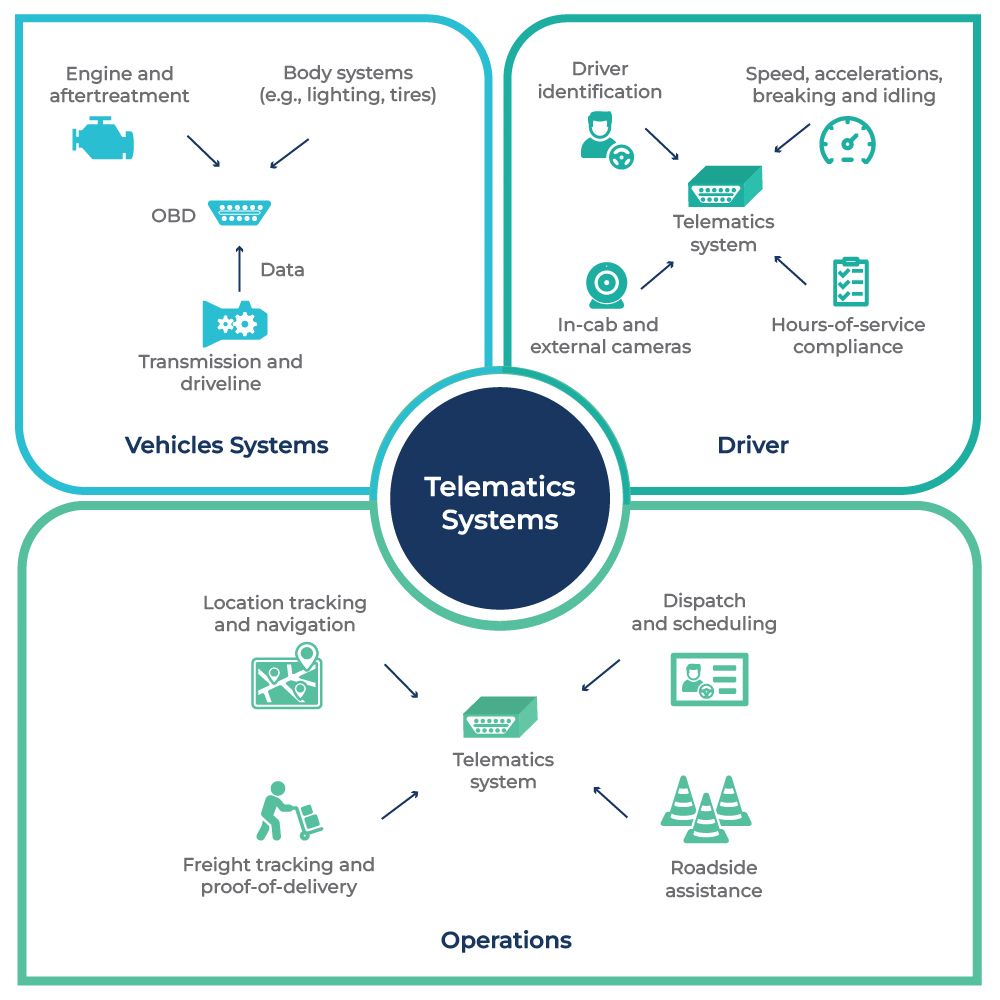

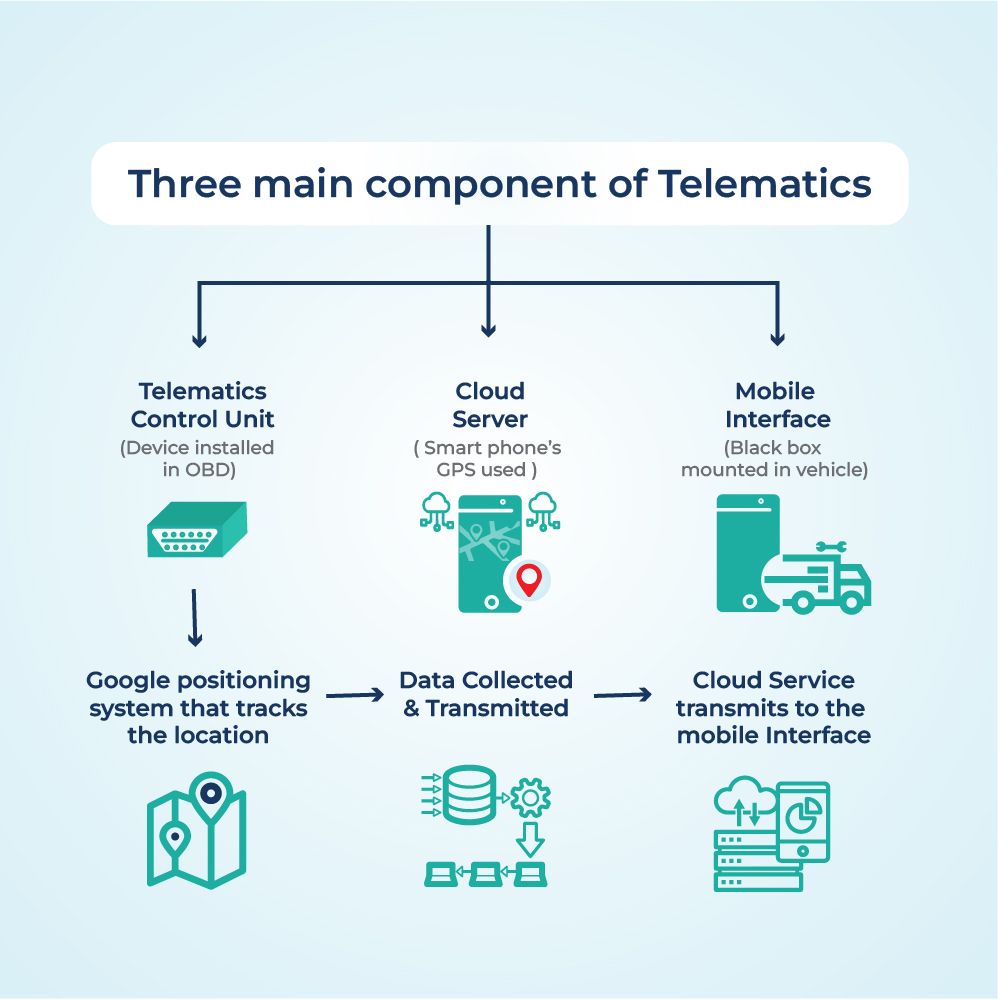

A telematics device is mounted in the vehicle. This device measures speed, distance traveled, location, frequency of driving, acceleration, breaks, how many breaks you take on a long trip and how long they are, etc., are measured and recorded. All of this information helps the insurance provider in determining the risk based on your driving style and adjusting the premium to reflect safe driving practices.

Advantages of Telematics-Based Auto Insurance

- Telematics-Based Insurance benefits both Insurer and Insured

- Accurate Risk Management

- Prompts better driving behavior.

- Saves fuel and Repair costs.

- Data-based inspection lowers the business costs.

- Reduces vehicle thefts and easy to identify fraud claims.

- Real-time helps in emergency warning signals during an accident.

- Pay as You Drive (PAYD)- Based on actual distance traveled and data is gathered from the odometer reading.

- Pay How You Drive (PHYD)- Based on driving patterns including braking, acceleration and hard cornering etc.

- Pay as You Go (PAYG)- Based on various data points such as driving patterns, time taken to cover distance and historic risk of the road etc.

- Pay Per Mile(PPM)- Based on the number of miles driven.

The big question: Indian Scene for Telematics-Based Insurance

Currently, Telematics-Based Insurance is not generally accessible in India. However, only a small number of insurance companies in India supply it and in the row “Edelweiss General Insurance” becomes India’s first company to launch mobile telematics based motor insurance - Switch. Switch is a fully digital, telematics-based auto insurance policy that, when a vehicle is moved, instantly activates insurance

Telematics is now being primarily used in India by fleet management businesses like taxi services, logistics firms, etc. It helps track journey duration, time, route, and driving behavior while keeping their vehicles connected to a central server.

How Telematics Insurance Premiums Are Calculated

Understanding the Risk Scoring Process

One of the biggest differences between traditional insurance and telematics insurance is the way premiums are calculated. Instead of relying solely on historical claims, vehicle type, or driver demographics, telematics insurance continuously evaluates real-time driving data to generate a dynamic risk score. This score helps insurers determine whether a driver presents a low, moderate, or high level of risk.

Modern telematics platforms collect data through GPS trackers, onboard diagnostics (OBD), connected vehicle systems, and IoT-enabled sensors. This information allows insurers to move from generalized pricing models to personalized insurance plans based on actual vehicle usage and driver behaviour.

Key Factors That Influence Insurance Premiums

Insurance providers generally evaluate multiple parameters before determining the final premium:

- Driving Frequency: Vehicles that are driven less frequently often have lower accident exposure and may qualify for lower premiums.

- Trip Duration: Long-distance journeys increase vehicle exposure on the road, while shorter and well-planned trips generally reduce overall risk.

- Road Type: Driving primarily on highways may present different risk levels compared to operating in congested urban traffic or accident-prone routes.

- Driver Behaviour Patterns: Consistent driving habits over time indicate lower operational risk compared to irregular or aggressive driving.

- Vehicle Maintenance Records: Connected telematics systems can identify overdue maintenance, engine diagnostics, battery health, and warning alerts that may increase accident probability if ignored.

- Incident History: Previous collision events, emergency braking records, and repeated safety violations help insurers build an overall driver risk profile.

Why Dynamic Risk Scoring Matters

Dynamic pricing benefits both insurers and fleet operators because premiums become more transparent and performance-driven. Instead of paying a fixed premium regardless of driving quality, businesses that invest in driver training, preventive maintenance, and route optimisation can gradually improve their risk score. This encourages safer driving habits while allowing insurers to price policies more accurately based on measurable operational data rather than assumptions.

Traditional Commercial Vehicle Insurance vs Telematics Insurance

As commercial transportation becomes increasingly connected, businesses are shifting from conventional insurance models to usage-based insurance that rewards operational efficiency and safe driving. The following comparison highlights how both approaches differ across important operational parameters.

| Feature | Traditional Commercial Vehicle Insurance | Telematics-Based Insurance |

|---|---|---|

| Premium Basis | Fixed using historical records and vehicle information | Continuously adjusted using real-time driving data |

| Risk Evaluation | Based on historical claims and demographics | Based on actual driving behaviour and vehicle usage |

| Driver Monitoring | Not available | Real-time monitoring through telematics devices |

| Safe Driving Rewards | Minimal | Premium discounts for responsible driving behaviour |

| Fleet Visibility | Limited | Live visibility into vehicles, drivers, and trips |

| Accident Investigation | Manual inspection and documentation | Supported by GPS, trip history, and telematics records |

| Fraud Prevention | Comparatively difficult | Easier through verified vehicle movement data |

| Vehicle Diagnostics | Not included | Available through connected telematics systems |

| Operational Insights | Not available | Actionable analytics for improving fleet performance |

| Best Suited For | Individual vehicle owners and conventional fleets | Logistics companies, transport businesses, and enterprise fleets |

Choosing the Right Insurance Model

For businesses operating commercial vehicles, telematics insurance offers significantly greater operational value than traditional insurance. By linking insurance premiums with actual fleet performance, companies can actively reduce costs through safer driving practices, preventive maintenance, route optimisation, and improved vehicle utilisation. This performance-based approach supports long-term operational efficiency while creating stronger collaboration between insurers and fleet operators.

How Telematics Data Improves Insurance Claims Investigation

From Accident Reporting to Data-Driven Claims

Traditional insurance claims often depend on manual inspections, witness statements, photographs, and physical evidence to determine fault. While these methods remain important, they may not always provide a complete picture of what actually occurred during an accident. Telematics insurance introduces objective, real-time data that enables insurers to investigate claims with greater speed and accuracy.

Every journey generates a digital record that includes vehicle location, speed, travel direction, timestamps, and driving behaviour immediately before, during, and after an incident. This information helps insurers reconstruct accident events using factual operational data instead of relying solely on subjective accounts.

How Telematics Supports the Claims Process

Telematics data enhances different stages of claim verification by providing valuable operational insights, including:

- Accurate Location Verification: GPS records confirm where and when an accident occurred.

- Impact Analysis: Sudden changes in speed, harsh braking events, and collision alerts help estimate the severity of an incident.

- Trip Timeline Reconstruction: Insurers can review the complete sequence of events leading up to an accident, improving investigation accuracy.

- Driver Behaviour Assessment: Driving patterns before the collision help determine whether speeding, aggressive acceleration, or unsafe manoeuvres contributed to the incident.

- Faster Claims Validation: Digital evidence reduces the time required to verify accident details, enabling quicker claim approvals.

- Fraud Detection: False accident claims, duplicate claims, or fabricated vehicle movements become easier to identify using telematics records.

Benefits for Fleet Operators and Insurers

The use of telematics during claims investigation creates advantages for every stakeholder involved.

For fleet operators:

- Faster claim settlements reduce vehicle downtime.

- Accurate incident records simplify communication with insurers.

- Reliable evidence helps resolve liability disputes more efficiently.

- Lower fraudulent claims contribute to better long-term insurance performance.

For insurance providers:

- Improved underwriting accuracy based on verified operational data.

- Reduced investigation costs through automated data collection.

- Better fraud prevention using real-time vehicle records.

- More consistent and transparent claims assessment processes.

As connected vehicle technology continues to evolve, telematics is expected to play an increasingly important role in modern insurance ecosystems. Rather than serving only as a tool for premium calculation, it is becoming an essential component of risk assessment, accident analysis, and evidence-based claims management, making commercial vehicle insurance more transparent, efficient, and data-driven.

Conclusion

In order to gain a clearer understanding of a driver's risk, insurers have now formed new sources of rating information. Regardless of the driver's past driving record, you can lower your auto insurance price by maintaining the driving patterns. Now that the driving behavior can be monitored in real-time, the insurance rate will not be based on the historical risk score. Therefore, real-time tracking motivates drivers to drive more cautiously, which results in fewer losses. The benefits of telematics-based insurance extend beyond the insurer and the policyholder to a wide range of stakeholders, including automakers. Therefore, telematics technology has a very broad use and can be utilized to increase revenue.

Frequently Asked Questions

What is telematics insurance and how does it work for commercial vehicles?

Telematics insurance is a usage-based motor insurance model where insurance premiums are determined using real-time driving and vehicle data instead of relying only on historical claims or fixed vehicle information. A telematics device, GPS tracker, mobile application, or an integrated connected vehicle platform continuously records operational information such as mileage, route history, driving time, braking patterns, acceleration, speeding events, idle time, and vehicle diagnostics. Insurance companies analyse this information to understand the actual risk associated with a vehicle or fleet before determining premiums.

For commercial fleets, telematics insurance provides far greater transparency than conventional insurance because businesses can actively influence their insurance costs through safer driving practices and better fleet management. Rather than paying the same premium every year regardless of operational performance, fleet owners are rewarded for maintaining safer vehicles and responsible drivers.

Telematics insurance is particularly valuable for:

- Logistics companies managing large commercial fleets.

- Transport businesses operating across multiple Indian states.

- Taxi and passenger transport operators.

- Cold chain and FMCG distribution companies.

- E-commerce delivery fleets.

- Construction and mining vehicle operators.

Across India, especially in logistics hubs such as Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune, businesses are increasingly adopting GPS-enabled fleet management systems alongside telematics insurance to reduce accident frequency, improve driver accountability, lower insurance claims, and optimise operational costs. As connected mobility continues to evolve, telematics insurance is becoming an important component of modern commercial fleet risk management.

What are the different types of telematics insurance available in India?

Telematics insurance is available in several usage-based models, each designed to match different driving patterns and business requirements. Instead of offering a single premium structure, insurers use different pricing approaches depending on how vehicles are used. Although adoption is still growing in India, many insurance providers are gradually introducing telematics-enabled commercial vehicle policies as digital fleet management becomes more common.

The most common telematics insurance models include:

- Pay As You Drive (PAYD): Premiums depend primarily on the number of kilometres travelled. Businesses with lower annual vehicle utilisation often benefit the most.

- Pay How You Drive (PHYD): Insurance costs depend on driving behaviour, including speeding, harsh braking, rapid acceleration, cornering and overall driving discipline.

- Pay As You Go (PAYG): Premiums are calculated using multiple operational parameters including distance travelled, vehicle usage frequency, route conditions and driving behaviour.

- Fleet-Based Telematics Insurance: Designed specifically for commercial fleets where insurers evaluate the overall fleet performance rather than individual vehicles alone.

Businesses in Delhi NCR, Mumbai, Bengaluru, Pune and Gurgaon often prefer fleet-based telematics insurance because it integrates with existing GPS vehicle tracking systems and fleet management software. This allows businesses to monitor drivers, improve compliance, reduce fuel wastage and negotiate more competitive insurance premiums over time. As India's connected vehicle ecosystem matures, insurers are expected to introduce more customised policies tailored for logistics, transportation and enterprise fleet operators.

Which is the best telematics insurance solution for logistics companies in India?

There is no single telematics insurance solution that is ideal for every business because the right choice depends on fleet size, operating region, vehicle type, and existing fleet management infrastructure. Instead of selecting an insurance policy based only on price, logistics companies should evaluate how well the insurer integrates with GPS tracking systems, driver monitoring platforms and fleet analytics solutions.

The best telematics insurance solution generally offers:

- Real-time GPS vehicle tracking.

- Driver behaviour monitoring.

- Accident alerts and emergency response.

- Vehicle health diagnostics.

- Trip history and route analytics.

- Claims assistance using telematics data.

- Fleet-wide performance dashboards.

- Easy integration with transportation management software.

For businesses operating across Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune, selecting an insurer that supports commercial fleet operations is usually more beneficial than choosing a generic personal vehicle insurance plan. Large logistics companies should also compare claim settlement efficiency, digital policy management, analytics capabilities, customer support and long-term premium savings rather than focusing solely on annual insurance costs.

As telematics adoption continues to grow across India's logistics industry, businesses combining fleet management software with telematics-enabled insurance are generally better positioned to improve safety, reduce operational risks and lower their total cost of ownership over time.

How much does telematics insurance cost for commercial vehicles in India?

The cost of telematics insurance in India varies depending on factors such as fleet size, vehicle category, annual mileage, driver behaviour, claims history, and the level of telematics integration. Unlike conventional commercial vehicle insurance, telematics insurance uses real-time operational data to determine premiums, allowing businesses to pay based on actual risk rather than standard assumptions. As a result, companies with disciplined drivers and well-maintained fleets often receive more competitive insurance pricing over time.

Although pricing differs between insurers, businesses can generally expect the following:

- Light commercial vehicles typically have annual premiums ranging from ₹18,000 to ₹45,000, depending on vehicle type and coverage.

- Medium and heavy commercial vehicles may range between ₹45,000 and ₹1.50 lakh+ annually based on vehicle value and operational risk.

- Fleet operators implementing telematics may reduce renewal premiums by approximately 10%–25% over time through safer driving records and fewer claims.

- Advanced telematics devices or software integrations may involve additional implementation costs if businesses do not already use GPS-based fleet management systems.

In logistics hubs such as Delhi, Gurgaon, Mumbai, Bengaluru and Pune, many transport companies evaluate the total return on investment rather than insurance cost alone. Lower accident rates, improved fuel efficiency, quicker claims processing and reduced vehicle downtime often deliver greater long-term savings than the annual premium itself. Businesses should therefore compare insurers based on overall fleet value rather than simply choosing the lowest-priced policy.

Can telematics insurance help logistics companies reduce operating costs in Delhi, Gurgaon, Mumbai and other Indian cities?

Yes. While telematics insurance is primarily designed to improve risk assessment, it also contributes significantly to lowering overall fleet operating costs. Commercial fleets operating in metropolitan regions often face challenges such as traffic congestion, accident risks, fuel theft, vehicle misuse and higher insurance claims. Telematics addresses these issues by combining GPS tracking, driver behaviour monitoring and operational analytics into one connected system.

For logistics companies operating in Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune, telematics insurance creates measurable business value beyond insurance savings.

- Encourages safer driving through continuous driver performance monitoring.

- Reduces accident frequency and repair expenses.

- Improves route planning to minimise unnecessary mileage.

- Supports predictive vehicle maintenance using connected diagnostics.

- Accelerates insurance claim verification through GPS and trip history.

- Reduces fraudulent claims using real-time vehicle data.

- Improves fleet utilisation by identifying operational inefficiencies.

- Strengthens compliance with internal safety policies.

For companies managing hundreds of commercial vehicles across multiple states, these operational improvements often generate savings that exceed the direct reduction in insurance premiums. As India's logistics sector continues adopting AI-driven fleet management and connected mobility technologies, telematics insurance is increasingly viewed as a strategic business investment rather than simply an insurance product.

How should businesses choose the best telematics insurance provider in India?

Selecting a telematics insurance provider requires evaluating much more than premium pricing. Businesses should consider whether the insurer supports long-term operational improvement through technology, analytics and responsive claims management. The ideal provider should complement an organisation's fleet management strategy while offering scalable insurance solutions as the fleet grows.

Before selecting a provider, businesses should compare the following factors:

- Compatibility with existing GPS tracking or fleet management software.

- Real-time driver behaviour analytics.

- Availability of digital policy management and online claim tracking.

- Accuracy of accident detection and incident reporting.

- Customer support and claim settlement efficiency.

- Coverage flexibility for mixed commercial fleets.

- Availability of usage-based pricing models such as PAYD or PHYD.

- Reporting dashboards for fleet managers.

- Data privacy and cybersecurity standards.

- Experience serving logistics and transportation businesses.

Companies located in Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune often benefit from insurers that understand large commercial fleet operations and provide dedicated support for logistics businesses. Instead of choosing the cheapest option, decision-makers should evaluate long-term value, technology capabilities and operational benefits. A provider that enables safer driving, faster claims, lower downtime and improved fleet visibility typically delivers significantly higher returns over the life of the insurance policy.

How is telematics insurance expected to evolve in India over the next few years?

Telematics insurance is expected to play a much larger role in India's commercial vehicle insurance market as connected mobility, artificial intelligence (AI), Internet of Things (IoT), and digital fleet management become more widely adopted. While telematics-based insurance is currently offered by a limited number of insurers, industry experts expect usage-based insurance products to become increasingly common for logistics companies, transport operators, passenger fleets, and enterprise vehicle owners.

Several trends are expected to drive this growth:

- Greater adoption of GPS-enabled commercial vehicles across India.

- Expansion of AI-powered driver risk scoring models.

- Increasing use of video telematics for accident verification.

- Growth of electric commercial vehicle fleets requiring new insurance models.

- Better integration between fleet management software and insurance providers.

- More personalised insurance products based on actual vehicle usage.

- Faster digital claims processing supported by connected vehicle data.

- Improved regulatory support for technology-driven motor insurance.

Major logistics centres such as Delhi, Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune are likely to witness faster adoption because businesses in these regions already rely heavily on GPS tracking, transportation management systems, and fleet analytics. As insurers continue investing in predictive analytics and connected vehicle ecosystems, telematics insurance will move beyond premium calculation and become an important component of fleet safety, operational efficiency, and long-term risk management. Businesses that begin adopting telematics early are likely to benefit from improved fleet visibility, reduced operational costs and more competitive insurance pricing over time.

What challenges should businesses consider before implementing telematics insurance?

Although telematics insurance offers numerous operational and financial benefits, businesses should understand the implementation challenges before adopting a usage-based insurance model. Successful implementation depends not only on installing telematics devices but also on ensuring drivers, fleet managers and insurance providers effectively use the collected data to improve operational performance.

Some of the most common challenges include:

- Initial investment in GPS devices or telematics-enabled hardware if a fleet is not already digitally connected.

- Employee concerns regarding driver privacy and continuous monitoring.

- Requirement for reliable internet connectivity and uninterrupted data transmission.

- Integration with existing fleet management software and ERP systems.

- Training fleet managers to interpret telematics reports and performance dashboards.

- Selecting an insurance provider that supports transparent data usage policies.

- Ensuring cybersecurity measures are in place to protect connected vehicle data.

- Managing change across large fleets where drivers may initially resist behavioural monitoring.

Businesses operating in Delhi NCR, Gurgaon, Mumbai, Bengaluru and Pune should also evaluate the scalability of their telematics solution as fleet sizes increase. Choosing a technology partner that provides regular software updates, reliable customer support and seamless integration with insurance providers can significantly simplify implementation. While these challenges require planning, the long-term advantages—including improved safety, reduced claims, better operational visibility and lower insurance costs—often outweigh the initial investment.

Is telematics insurance suitable for small businesses and growing transport companies in India?

Yes. Telematics insurance is no longer limited to large enterprise fleets. Small transport companies, regional logistics providers, fleet startups and businesses operating a limited number of commercial vehicles can also benefit from usage-based insurance. As cloud-based fleet management platforms become more affordable, smaller businesses now have access to technologies that were previously available only to large logistics organisations.

Telematics insurance can be particularly beneficial for growing businesses because it helps establish safer operational practices from the beginning while reducing long-term insurance risks.

- Encourages responsible driving through continuous performance monitoring.

- Improves vehicle utilisation and trip planning.

- Supports preventive maintenance by identifying vehicle issues early.

- Provides accurate operational records for insurance claims.

- Reduces unnecessary fuel consumption through better driving behaviour.

- Helps businesses build stronger insurance histories for future policy renewals.

- Improves customer service by enabling better vehicle tracking and delivery visibility.

- Creates measurable operational data that supports future business expansion.

Small fleet operators in Delhi, Gurgaon, Mumbai, Pune and Bengaluru increasingly use telematics alongside GPS vehicle tracking to improve profitability while maintaining competitive operating costs. As insurers continue expanding telematics-based products across India, businesses of all sizes can benefit from personalised insurance pricing, improved safety standards and more efficient fleet operations without requiring enterprise-scale infrastructure.

{kind=link}